Some of my favorite take-aways from our Payment’s Operator Series April 2026 event week on “Rethinking the Merchant Stack for Agentic Commerce”.

The merchant perspective:

– AI referrals disproportionately drive net new customers

– Conversion overall much higher compared to search but payment abandonment is higher

– Payment drop could be due to mix of new customers, lack of pricing clarity in initial AI search (not sure why)

– Accurately tracking AI referal is hard, you are probably significantly under-counting, a good tip is to ask customer’s post check-out how they heard of you

– AI queries are much longer and open ended. At Seat Geek it’s ‘What shows are playing in my town this weekend that could be good for a date night?’ vs google ‘Tickets for Tame Impala Seattle’

– For recommendations AI isn’t just sourcing from a few top sites like reddit, it’s pretty fragmented and segment specific

– AI recommendations are more deterministic than you think. There is variance if you ask only a few times but recommendations cluster around a stable distribution of responses if you ask 20 times.

Insights from the network:

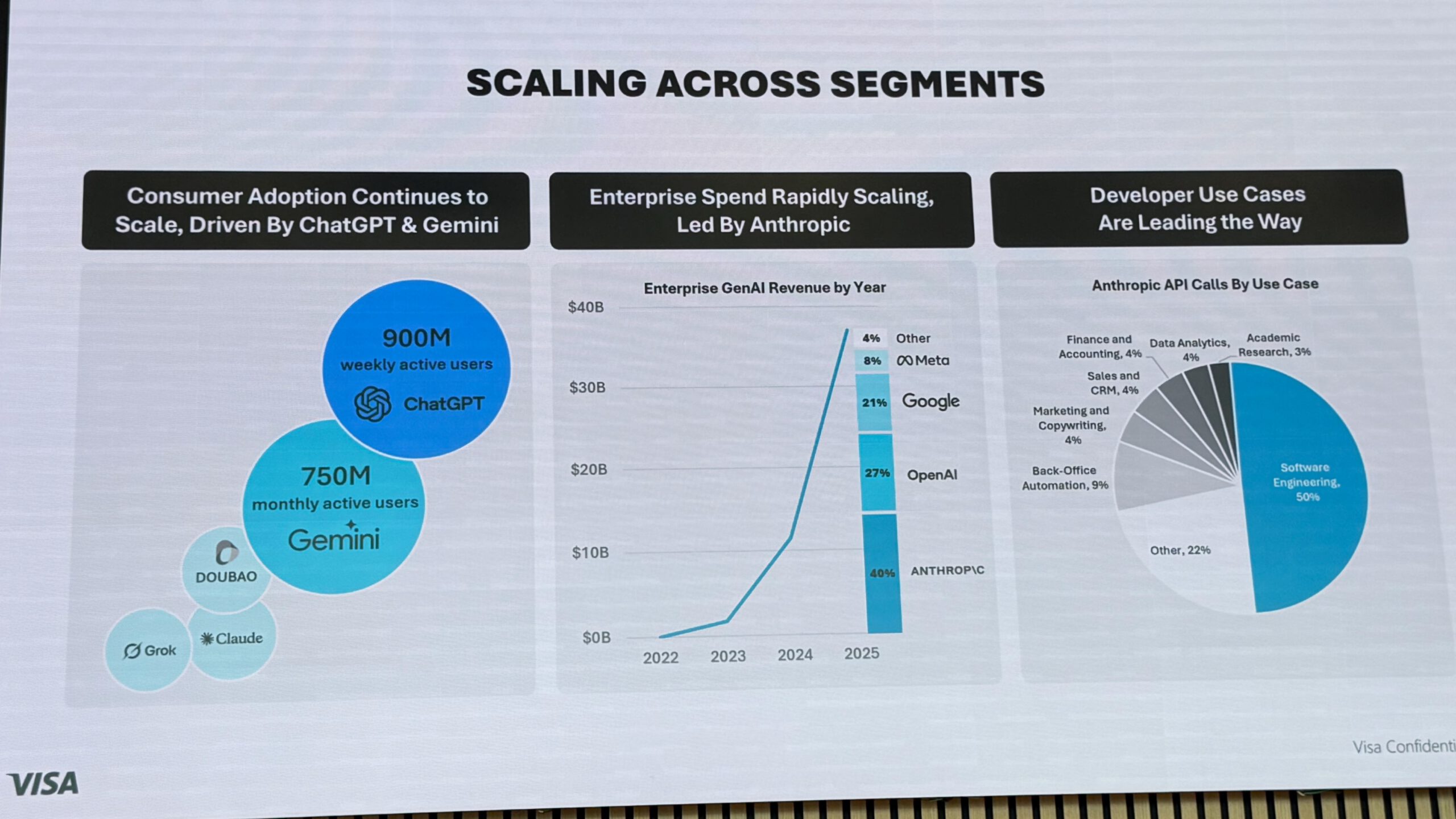

– AI is the fastest growing digital channel (by user adoption) we’ve ever seen

– The biggest power usecases (by token consumption) are Software development (50%), Back-office-Automation (9%), Marketing+Sales/CRM (8%), Finance/accounting (4%), Data Analytics (4%), long tail of everything else 22%. So hint: if you wanted to guess where true angent to agent commerce is going to take off first, maybe think about these segments and usecases first?

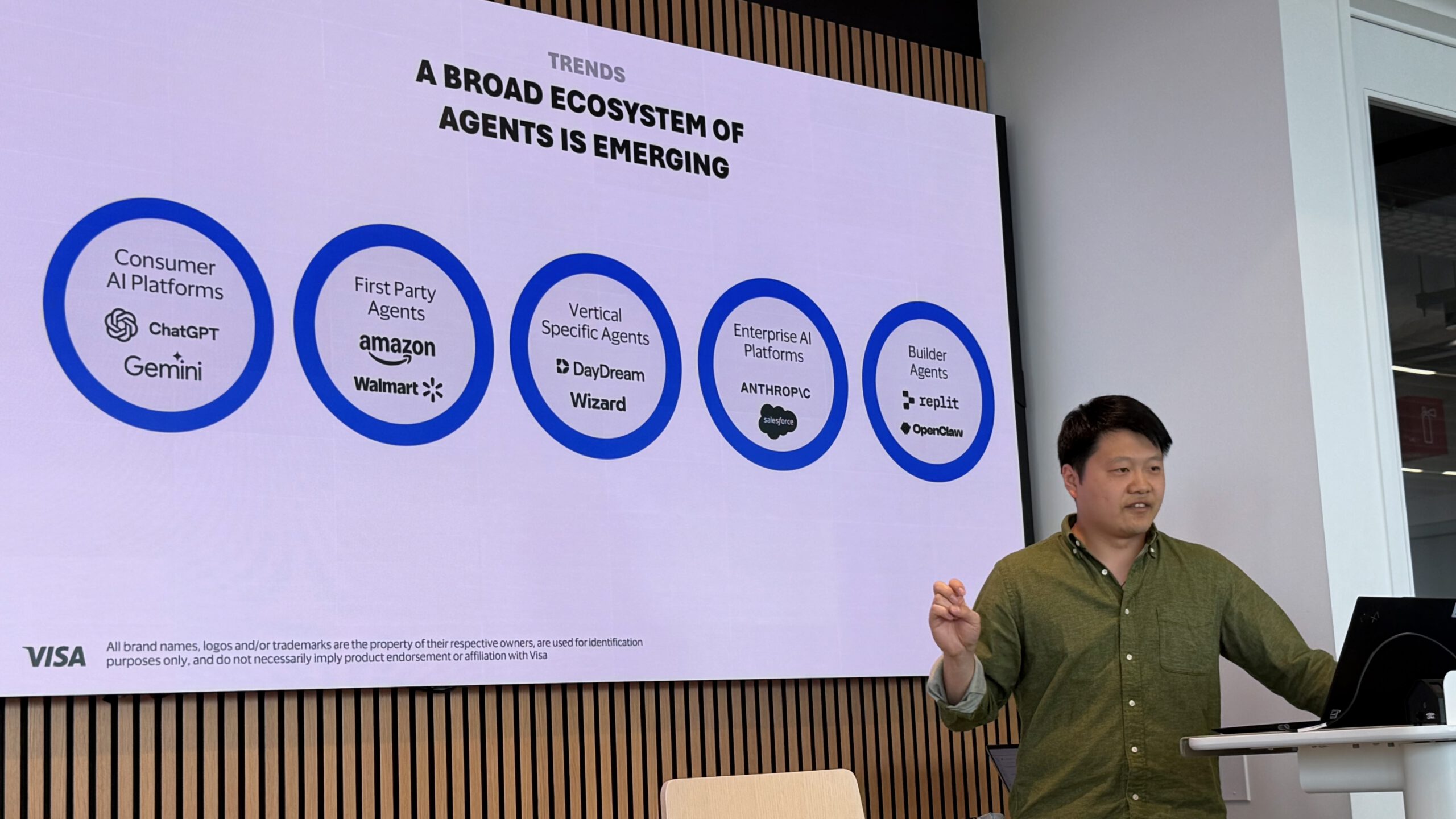

– ‘Agentic Commerce’ depends on what surface you are talking about. Alex Chiang models at least 5 distinct flavors: Consumer Platforms (GPTs), First Party Agents (Like Amazon Rufus), Vertical Specific Agents, Enterprise AI Platforms, and “Builder Agents” (e.g Claws)

AI Transformation Perspective:

– Don’t confuse Agentic AI projects with magically solving all your business process automation gaps, if anything fix the latter first as a pre-requisite

– Most people aren’t ready to fully let AI take the wheel on decision making, and particularly on pressing the buy button (yet)

– But it’s highly person and context specific on when you trust the AI more than yourself not to make mistakes, and inevitably we’re all going to start leaning on AI more and more. Esp as the world itself gets overrun with more complexity, AI fakes and new threat environments, it may be crazy not to rely on your own set of agents.

– AI is exploding our ability to generate content, products and new software, which requires new roles and organizational thinking. Editorial and curation skills become more important than ever, it’s not getting cheaper to support in production, to secure them and to go to market. But prototypes are 1000x easier to build. [my view: not launching 90% of your AI prototypes is expected behavior!]

Thanks for Visa for graciously hosting, thanks to Grace Wu for pulling another great event together as well as inviting me to MC